Restaurant ordering technology is consolidating

Episode 23 Quick Summary November 2021

Restaurant order handling is, for e-commerce technology providers, as big a market opportunity as meal delivery marketplaces

Point Of Sale (‘POS’) and workflow technologies have been fragmented but are now consolidating, albeit in an open ecosystem

Restaurants are being enabled to handle more orders and to free themselves from high marketplace fees by paying software subscriptions and reduced transaction fees

Delivery platforms will have a looser hold over restaurants but are also integrating with emerging restaurant technology so that they can stay relevant

Full restech consolidation article available to paid Aggregators subscribers.

In 2019, for the first time in history, the restaurant industry’s share of household spending on food exceeded the share from food stores, says the US National Restaurant Association. Yet, traditionally, restaurants spend only a fraction of what food stores spend on technology and e-commerce. But through the pandemic there has been a burst of digital adoption.

Food marketplace and delivery platforms have been a saviour for many restaurants. Nevertheless, restaurants are increasingly seeking to use more technology to control, and diversify from, their dependence on the platforms. Most restaurants nowadays pursue not only multiple ways to offer food, but also multiple channels to attract customers. From quick service restaurants to the high-end fine dining establishments, most would now consider themselves to be omnichannel...enabled by an array of e-commerce services and software subscriptions to control their operations.

Olo and Toast, together touch, in the US, around the same volume of orders, as the two leading delivery platforms, DoorDash and UberEats combined.

The market for restaurant order management tools to either complement or replace marketplace platforms is comparable in size to the better-known marketplace opportunity. The two leading order management providers, Olo and Toast, together touch, in the US, by my reckoning, around the same volume of orders, roughly 2½bn a year, as the two leading delivery platforms, DoorDash and UberEats combined. Comparison of market size is not straightforward, because order management is paid for in (largely) fixed subscriptions whereas marketplace is paid for in transaction fees which are a fraction of the commonly referenced ‘gross meal value’ market size. My alternative comparison of market sizes and restaurant take rates in the UK and US focuses on revenue to the service providers, not gross meal value spent by the consumers.

Full analysis in the restech consolidation Aggregators paid subscriber article.

In marketplace and delivery platforms, the US market is much more mature than the UK ($11bn compared with $4bn), but in order management there is less difference (US $5bn, UK $3½bn), because there are a higher proportion of UK own-delivery restaurants needing order management to control their delivery process. Relative to the size of the economy, the UK’s standalone demand aggregation channels, including direct to consumer, are larger. Order management tools have lower take rates but greater coverage, because they operate on all order channels, not just aggregator channels

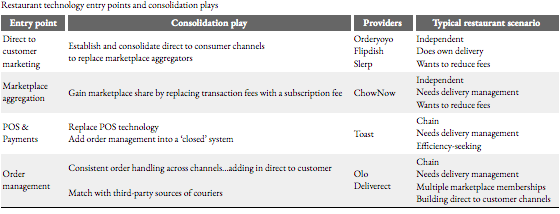

In these times of punitive marketplace transaction fees, paying by the ‘fixed’ software route is starting to look attractive. The various ‘direct to customer’ channels on offer don’t guarantee orders as consistently as marketplaces do, but they do equip restaurants to grow and control their own demand channels. Right now, these different propositions mostly complement each other but are starting to expand and overlap. Providers, based on their original footholds, are offering different consolidations to capture more restaurant spend.

The restaurant POS hardware and software market remains very fragmented. The long tail of small restaurants have little appetite for new or replacement equipment. Global chains, too, have multiple POS systems, from household names like Oracle to retail niche providers, even within national markets. Toast is rare in having its own POS hardware and software offering as part of a closed order management system. Its investment in POS and payments is far-sighted (like Etsy in craft and gifting marketplaces). Olo, by contrast, does not offer POS but integrates a range of third-party POS as well as upstream demand aggregators and downstream delivery providers, amidst an open system of over 100 technology partners. Integrations will broaden and deepen as an open ecosystem evolves - one which Olo will rely upon more than Toast.

Fees will migrate from transaction fees to software and service subscriptions (except for payments processing fees), giving restaurants more control and relieving the pressure from government regulators.

Just Eat in the UK saw better restaurant integration contributing to a rise in 6-month repeat rate from 17% to 25% over the course of two years.

Direct to customer enablers will be attractive in the short-term to fee-sensitive independent restaurants, but it will be a struggle to scale new direct online channels outside of the marketplaces, particularly as Google and Apple are now restricting online consumer targeting via cookies. Delivery platforms have recognised the threat to their business models from low repeat rates as restaurants seek more direct channels. They are responding by integrating with order management, although with POS systems they will continue to be selective in their integration investments. Just Eat in the UK is starting to see results, with better restaurant integration contributing to a rise in 6-month repeat rate from 17% to 25% over the course of two years. Platforms will accommodate restaurants that want to diversify channels and independently source delivery capacity.

Aggregators will revisit this fast-developing restaurant technology ecosystem in a few episodes’ time, but first we will check in on the state of labour costs in the leading delivery platforms.